Two important questions for readers. One here. One later.

Question #1: What would you think if I told you the CEO of a business that had to secure a $1 billion loan to stave off bankruptcy got paid over $100 million dollars?

Well, it just happened.

Barry McCarthy, the CEO of Peloton (PTON), got paid over $100 million in 2022. Let that settle in. The CEO of a company that is now cutting 15% of its staff and securing a $1 billion loan with a 12% yield got paid over $100 million in a single year. Meanwhile, Barry McCarthy stepped down as CEO. Do you think he’s giving any of his compensation back to the company, the employees that lost their jobs or the investors that have lost billions by owning the stock? I don’t think so.

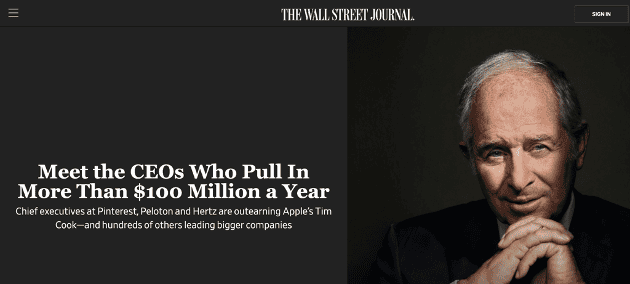

Figure 1: CEOs Who Got Paid over $100 Million

Image Source: Wall Street Journal

The problem here is not a new one. Executives are overpaid all the time – often by egregious amounts. The root cause of these horrific misallocations of capital is Boards of Directors, ie Compensation Committee members, that sign off on pay packages that allow these overpayments to happen. Most of the time, these overpayments occur because the Boards of Directors tie executive compensation plans to performance metrics, e.g Adjusted EBITDA, non-GAAP earnings, GAAP earnings, etc, that are not aligned with the best interests of the business or shareholders. In other words, if you pay executives to grow metrics that do not generate real profits, you’re paying them to run the business into the ground. That’s exactly what happened with Peloton, that’s what happened with WeWork’s “Community Adjusted EBITDA”. And, then, there’s Valeant’s “Cash Earnings”. We were attacked by many other analysts for writing that “Cash Earnings” were fake earnings. I hate to say it, but this happens far too often, and we always red flag stocks for companies that we see are paying executives based on metrics that are either super easy to manipulate or beat or both. Yet, there are troves of analysts on Wall Street and off Wall Street who support the use of these manipulated numbers.

And, it’s been going on for decades. Barry McCarthy’s compensation package was approved by Peloton’s Board of Directors. Were they meeting their Fiduciary Duties by approving such a pay package? Are they giving any of that $100 million back to the company, the employees that lost their jobs, or the investors that have lost billions by owning the stock? I don’t think so.

Is anyone held responsible?

No, not by regulators, the police, or anyone on Wall Street. Nope, not them.

The responsibility to hold these robbers accountable falls to you.

It’s the responsibility of all investors to vote with their capital.

Investors vote when they buy, sell, or hold a stock. When investors buy and hold, they implicitly endorse what management and the Board of Directors are doing and plan to do. Buying and/or holding says: “I trust you with my money.”

Now one could argue that buying or holding the stock means that investors just want to make money in the stock, but that answer does not hold water. It does not absolve them of the endorsement of management that owning the stock implies. The bottom line is that investors either let the company keep their money or not. If you let them keep it, you’re trusting them with it. It’s that simple.

Therefore, the only way to let management or the Board of Directors know you do not trust them or do not agree with how they are running the business is to sell the stock.

Question #2: what would you think if I put together a Model Portfolio of Attractive-or-better rated stocks with CEOs whose compensation was tied to ROIC?

When executives get paid to improve ROIC, they only make money when investors make money. This approach is called “tying compensation to shareholder value creation.” What a novel concept!!!!

How about we only pay bonuses to managers who increase the returns on the capital investors give them? I mean, that is the purpose of giving managers capital to begin with, no?

Tying executive compensation to creating shareholder value makes so much sense. Who can argue against it? Do any investors want to give money to managers who are going to use all or most of the capital to pay themselves huge bonuses while running the business and the stock into the ground?

The answer to that question is a big YES. Maybe, the investors do not realize it, but they are saying yes whenever they own the stocks of companies with poor executive compensation plans.

Maybe the investors just don’t care, or maybe, they just don’t know of any better alternatives.

That’s why I created a Model Portfolio of Attractive-or-better rated stocks with CEOs whose compensation is tied to ROIC. More details are here, and you can get a free sample report at the bottom of this page. Furthermore, I am such a big fan of this model portfolio and the idea of tying executive compensation to creating shareholder value that I did this special training on the topic.

Smart investing is not just about picking winners, it’s about avoiding the losers.

We try to help with both.

We warned investors to avoid Peloton before its IPO at ~$27/share (see our report). We made PTON Zombie Stock #3 in June of 2022 when it was at $11/share. Over the last few years, the stock has been as high as $160/share, and it is now trading under $4/share.

Figure 2: PTON’s Stock Price

Sources: Google Finance

We’re not the only people raising red flags. CNBC warned in this April 4. 2024 article: “Retailers like Peloton and Saks keep paying vendors late, signaling possible ‘financial distress’”. Uh, no duh. That’s what happens when your business doesn’t make any money for years on end.

The warning signs were there all along. Too bad more investors were not paying attention.

We, at New Constructs, are doing our best to get the word out and help investors. Our work on Peloton is proof of that effort.

And, we also help you find good stocks with our many Model Portfolios and Long Idea reports. Did you know that our research is proven superior in detailed studies published by Harvard Business School, Ernst & Young, MIT Sloan, The Journal of Financial Economics and the Indiana Kelley School of Business? Did you know that we’ve been the #1-ranked stock picker in multiple categories for 36 consecutive months on SumZero?

We regularly review our work and research on Long Ideas and Danger Zone Ideas with clients. We want you to know how much work we do! Here’s how we share our work:

- Free live Podcast every month. Next one is June 14th at 12pmET. Register here. Our last one was on May 10th at 12pmET. Get the free replay from our Society of Intelligent Investors (use this form to sign up for free) and ask questions and make requests anytime!

- Monthly Let’s Talk Long Ideas webinars where we do deep dives into our research, analytics, reverse DCF models and ideas for our Professional and Institutional clients. We just did one on May 8th at 3:30pmET. Replay is here for our Professional and Institutional clients.

- Sign up for my e-letters on our homepage.

Diligence matters,

David

This article was originally published on May 28, 2024.

Disclosure: David Trainer, Kyle Guske II, and Hakan Salt, receive no compensation to write about any specific stock, sector, style, or theme.

Questions on this report or others? Join our Society of Intelligent Investors and connect with us directly.