We closed this position on May 15, 2018. A copy of the associated Position Update report is here.

Market overreactions create buying opportunities. Despite improving profits, margins, and ROIC, the market recently punished this stock for “missing expectations.” Add in improving market conditions and prudent cost management to this backdrop of lowered expectations, and we believe the stock is positioned to outperform moving forward. Knoll Inc. (KNL: $24/share) is this week’s Long Idea and on April’s Most Attractive Stocks list.

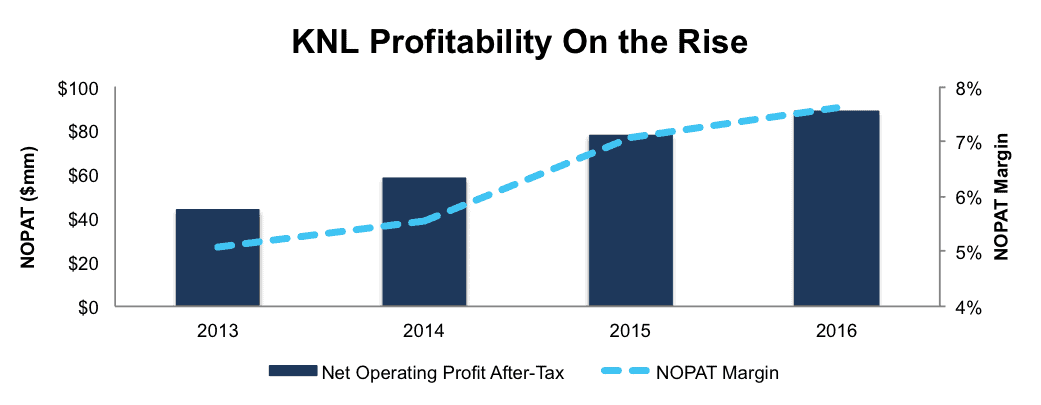

KNL’s Impressive Profit Growth

Since 2013, Knoll has grown after-tax profit (NOPAT) by 27% compounded annually to $89 million in 2016. The company has grown revenue by 11% compounded annually over the same time. Per Figure 1, the company’s NOPAT margin has improved from 5% in 2013 to nearly 8% in 2016. Longer-term, Knoll has grown NOPAT by 7% compounded annually since 2004.

Figure 1: KNL Profit Growth Since 2013

Sources: New Constructs, LLC and company filings

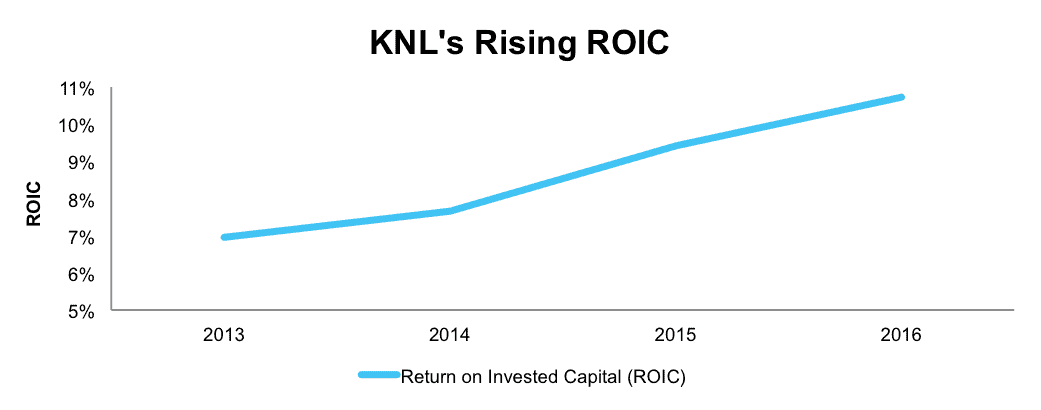

In addition to NOPAT growth, Knoll has generated a cumulative $85 million (6% of market cap) in free cash flow (FCF) over the past five years. Knoll has also exhibited good stewardship of capital amidst multiple acquisitions aimed at diversifying the business. Since 2013, Knoll has improved its return on invested capital (ROIC) from 7% to 11%, per Figure 2.

Figure 2: Knoll’s Good Stewardship of Capital

Sources: New Constructs, LLC and company filings

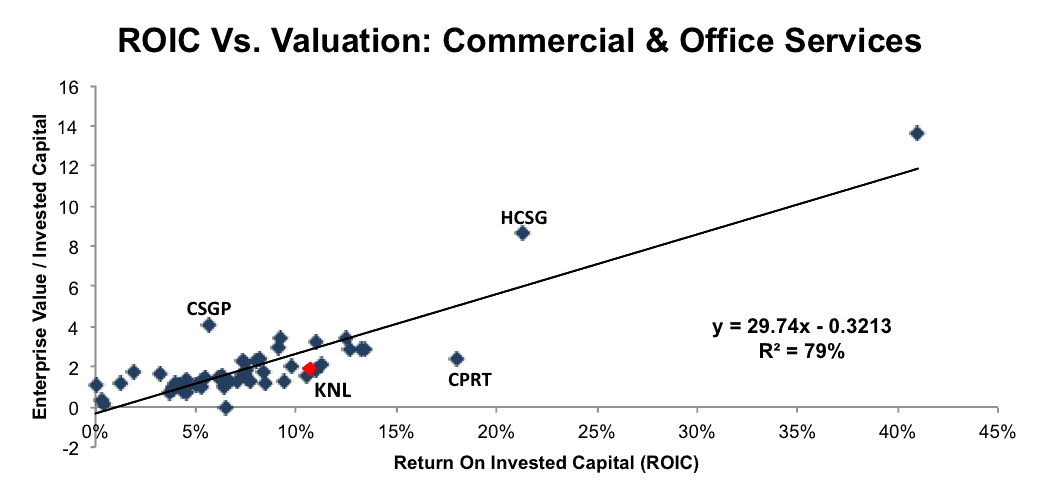

Improving ROIC Correlated With Creating Shareholder Value

Per Figure 3, ROIC explains 79% of the changes in valuation for the 52 Commercial & Office Services firms we cover. Despite KNL’s 11% ROIC, above the 8% average of the peer group, the firm’s stock trades at a discount to peers as shown by its position below the trend line in Figure 3. If the stock were to trade at parity with its peers, it would be at $40/share – 68% above the current stock price. Given the firm’s higher ROIC and impressive profit growth, one would think the stock would garner a premium valuation.

Figure 3: ROIC Explains 79% Of Valuation for Commercial & Office Services Firms

Sources: New Constructs, LLC and company filings

Leading Profitability Gives KNL A Competitive Advantage

In the commercial and residential furniture market, manufacturers compete largely on product design, quality, and price. Per Figure 4, KNL has the highest NOPAT margin and an equal ROIC versus peers, which include Herman Miller (MLHR), HNI Corporation (HNI), and Steelcase (SCS).

High margins allow KNL to invest more in market leading designs that meet the needs of a shifting mindset around workplace environments. At the same time, KNL’s profitability gives it flexibility to better withstand changes in raw materials prices or a downturn in the economy. Most importantly, KNL is also able to provide products at a lower price than competitors while maintaining profitability, an effective way to take market share.

Figure 4: KNL’s Top Profitability Among Competition

Sources: New Constructs, LLC and company filings.

Bear Concerns Ignore Improving Market Conditions

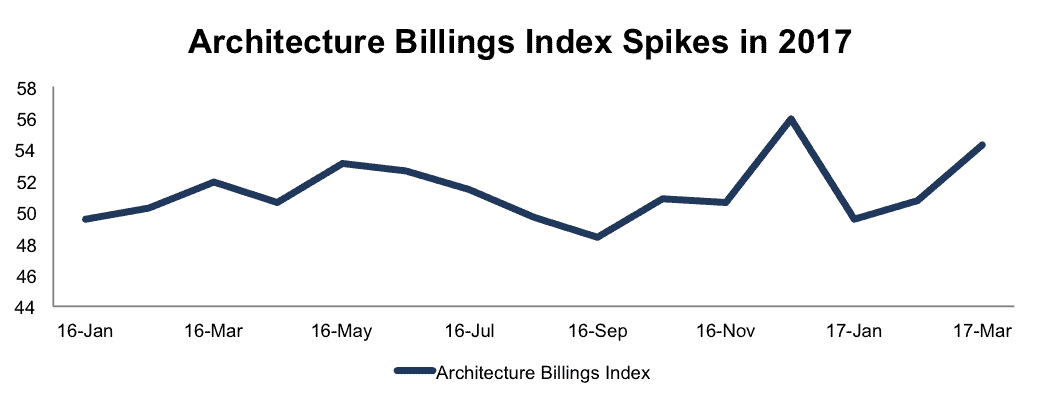

As a provider of furniture and accessories to commercial office spaces, KNL is reliant upon corporate spending, a strong job market, and growing economy. After a weak 4Q16, bears will argue that KNL’s best days are behind it. However, economic data, such as architecture billings, CEO confidence, and hiring plans, would show otherwise. Add in KNL’s ability to keep costs low, and the bear case begins to look rather weak.

The weak 4Q16, in which KNL missed revenue expectations, can largely be attributed to the presidential election. Across the board, KNL and its peers pointed to uncertainty regarding the trajectory of the economy as causing a weak fourth quarter. However, this weakness appears to have subsided now that the election is over. Figure 5 shows that the Architecture Billings Index, an indicator of nonresidential construction activity, has spiked in 1Q17. A score above 50 represents growth and March’s ABI score of 54.3 is up from not only January and February of this year, but also March of 2016.

Figure 5: ABI Suggests Increased Business Construction

Sources: New Constructs, LLC and American Institute of Architects

Additionally, the CEO Confidence Index, which measures CEO’s opinions on future economic and business conditions, reached 68 at the end of 1Q17. A score above 50 represents a positive opinion on the economy, and the 1Q17 score represents the highest rating since 2004. Furthermore, nearly two-thirds of those surveyed anticipate an increase in hiring in 2017, up from 30% of those surveyed in 2016. On the flip side, less than 10% expect a decrease in hiring in 2017, compared to 40% in 2016. Strong economic conditions bode well for KNL’s growth potential.

Apart from macro economic trends, KNL has focused on improving profitability, with specific focus on its Office segment, which was 62% of revenue in 2016. From investments in sales capabilities to lean manufacturing initiatives, KNL has improved its Office segment operating margin from 6% in 2014 to 10% in 2016. Company wide, the firm’s operating costs, such as selling, general, and administrative, have grown in line with revenue compounded annually since 2013. Prudent cost management moving forward will allow KNL to take advantage of the improving market and capitalize on increased business spending.

Lastly, KNL’s low valuation also undermines any bear argument. Despite rising sales, impressive NOPAT growth, and promising economic trends, KNL’s current valuation implies meager profit growth expectations, as we’ll show below.

Cheap Valuation Holds Significant Upside

Year-to-date, KNL is down 14% while the S&P is up 4%. This underperformance makes shares undervalued and presents a buying opportunity. At its current price of $24/share, KNL has a price-to-economic book value (PEBV) ratio of 1.1. This ratio means the market expects KNL to grow NOPAT by no more than 10% over the remainder of its corporate life. This expectation seems at odds with a firm that has grown NOPAT by 7% compounded annually since 2004.

However, if KNL can maintain 2016 NOPAT margins (8%) and grow NOPAT by 5% compounded annually for the next decade, the stock is worth $31/share today – nearly 30% upside. This scenario assumes KNL can grow revenue by consensus estimates in 2017 (<1%) and 2018 (5%), and 5% each year thereafter. With non-residential construction activity trending higher, potential changes to corporate tax spurring investment, and margin improvement initiatives, KNL could easily meet or surpass these expectations. Add in the 2.5% dividend yield and its clear why KNL is on this month’s Most Attractive Stocks List and could be an excellent portfolio addition.

Buy Backs Plus Dividend Could Yield 3%

In 2016, KNL repurchased over $5 million worth of stock, down from nearly $9 million in 2015. At the end of 2016, the company had over $32 million remaining under its current authorization. Going forward, if KNL were to average its 2015 and 2016 repurchase activity, the firm could repurchase a total of $7.1 million over four and half years. A repurchase of this size is 0.5% of the current market cap. When combined, Knoll’s 0.5% repurchase yield and 2.5% dividend yield offer investors a total potential yield of 3%.

Market Overreaction Sets Up Earnings Beat Opportunity

When KNL reported 4Q16 earnings, the stock fell 15% the following week. As noted above, the firm missed revenue expectations and investors overreacted to one weak quarter caused by election uncertainty. When looking below the top line miss, the firm continued to improve its fundamentals, including profits, margins, and ROIC. However, consensus estimates were quickly cut, setting up a scenario in which KNL has a great opportunity to beat these lowered expectations.

In order to beat expectations, KNL has focused on building out its business beyond the Office segment. With acquisitions of DatesWeiser and Vladimir Kagan in 2016, KNL aims to provide a more diversified offering of luxury furnishings through its Studio segment, which was 28% of revenue in 2016. The Studio segment’s operating margins of 17% are much greater than the Office segment so expanding this business line is key to growing profits.

Beating both top and bottom line expectations could be the catalyst that pushes the stock higher. When KNL reported 3Q16 results above consensus, the stock rose 11% over the next week. In 1Q16, when KNL again beat both top and bottom line expectations, the stock rose 7% in the following week.

With improving market conditions, including business activity and CEO confidence, and expansion of higher margin segments, KNL could be poised for another beat and subsequent increase in valuation. In the meantime, investors in this stock carry very low valuation risk and are rewarded with a potential 3% total yield given KNL’s history of dividends and share repurchases.

Executive Compensation Plan Could Be Improved But Raises No Alarms

Knoll’s executive compensation plan, which includes base salary, annual incentives, and long-term incentives, is largely tied to multiple metrics. Annual bonuses are tied to operating profit and supplemental goals at the discretion of the compensation committee. Long-term incentives consist of time-based shares and performance-based restricted stock units. Performance-based shares are tied to three-year operating profit targets and total shareholder return. We would prefer to see executive compensation tied to ROIC, since there is a strong correlation between ROIC and shareholder value, However, KNL’s current exec comp plan has not led to executives getting paid while destroying shareholder value. In fact, since 2010, Knoll’s economic earnings, the true cash flows of the business, have grown from $15 million to $40 million in 2016, a clear creation of shareholder value.

Insider Trends and Short Interest Are Minimal

Over the past 12 months, there have been 174 thousand insider shares purchased and 555 thousand insider shares sold. These sales represent 1% of shares outstanding. Additionally, short interest sits at 1.6 million shares, or 3% of shares outstanding.

Impact of Footnotes Adjustments and Forensic Accounting

Our robo-analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Knoll’s 2016 10-K:

Income Statement: we made $46 million of adjustments, with a net effect of removing $6 million in non-operating expense (1% of revenue). We removed $20 million in non-operating income and $26 million in non-operating expenses. You can see all the adjustments made to KNL’s income statement here.

Balance Sheet: we made $230 million of adjustments to calculate invested capital with a net increase of $191 million. The largest adjustment was $93 million due to operating leases. This adjustment represented 15% of reported net assets. You can see all the adjustments made to KNL’s balance sheet here.

Valuation: we made $412 million of adjustments with a net effect of decreasing shareholder value by $412 million. There were no adjustments that increased shareholder value. Apart from total debt, which includes the $93 million in operating leases noted above, one of the notable adjustments was $77 million in net deferred tax liability. This adjustment represents 6% of KNL’s market cap. Despite the net decrease in shareholder value, KNL remains undervalued.

Attractive Funds That Hold KNL

There are no funds that receive our Attractive-or-better rating and allocate significantly to Knoll Inc.

This article originally published on April 24, 2017.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Click here to download a PDF of this report.

Photo Credit: Photo by CafeCredit under CC2.0 (Flickr)

2 replies to "Industrials Stock With High Quality Risk/Reward"

I thought that I received a membership if I have a Scottrade account. I have four and have used them for 15 years.

Hi Douglas:

Thank you for your note.

Yes, your Scottrade account earns you a free Gold Membership $588/yr value.

Details on how to access your free Gold membership are here: https://staging.newconstructs.com/scottrade-info/