Eight new stocks make our Exec Comp Aligned With ROIC Model Portfolio this month. February’s Exec Comp Aligned With ROIC Model Portfolio was made available to members on 2/15/17.

Recap from January’s Picks

Our Exec Comp Aligned With ROIC Model Portfolio (+3.0%) outperformed the S&P 500 (+2.3%) last month. The best performing stock in the portfolio was Hasbro Inc. (HAS), which was up 19%. Overall, six out of the 15 Exec Comp Aligned With ROIC Stocks outperformed the S&P in January and 10 had positive returns.

Since inception, this model portfolio is up 25% while the S&P 500 is up 11%.

The success of the Exec Comp Aligned With ROIC Model Portfolio highlights the value of our forensic accounting (featured in Barron’s). Return on invested capital (ROIC) is the primary driver of shareholder value creation. By analyzing footnotes in SEC filings, we are able to calculate an accurate and comparable ROIC for 3000+ companies under coverage.

This Model Portfolio only includes stocks that earn an Attractive or Very Attractive rating and align executive compensation with improving ROIC. We think this combination provides a uniquely well-screened list of long ideas.

New Stock Feature for February: Plexus Corporation (PLXS: $57/share)

Plexus Corporation (PLXS), electronic manufacturing services provider, is one of the additions to our Exec Comp Aligned With ROIC Model Portfolio in February.

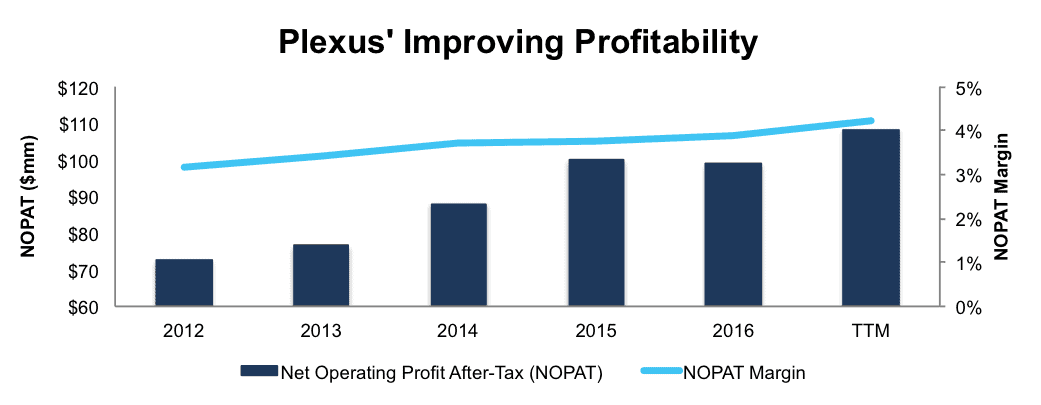

Since 2012, Plexus has grown after-tax profit (NOPAT) by 8% compounded annually to $99 million in 2016. NOPAT has grown to $108 million over the last twelve months (TTM). At the same time, the firm’s NOPAT margin has improved from 3% in 2012 to 4% TTM, per Figure 1.

Figure 1: NOPAT & NOPAT Margin Improvement

Sources: New Constructs, LLC and company filings

Plexus currently earns a 10% return on invested capital (ROIC) and has generated a cumulative $257 million in free cash flow over the past five years.

Executive Compensation Aligned With ROIC Creates Shareholder Value

ROIC and return on capital employed (ROCE), a similar measure to ROIC, have been part of Plexus’ executive compensation plan since 2004. In 2016, the annual cash incentive, which makes up 20% of executive pay, was based upon revenue and ROCE.

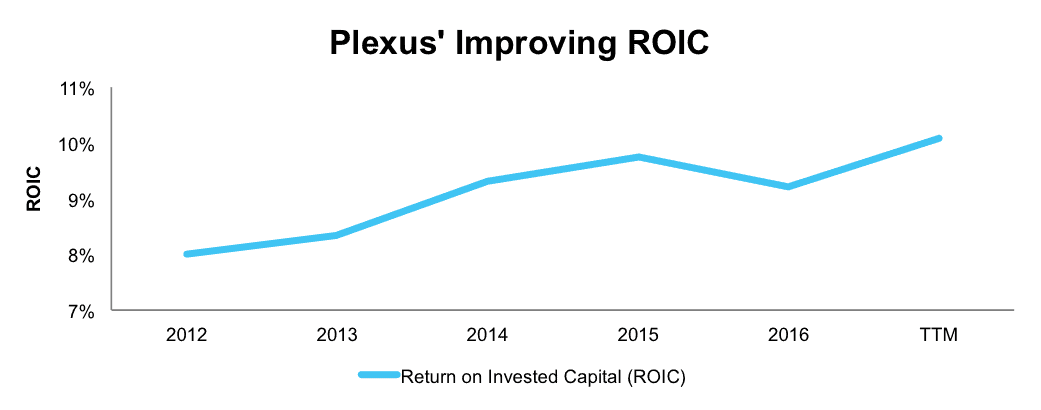

The focus on ROIC and ROCE helps make executives good stewards of investors’ capital. Per Figure 2, Plexus’ ROIC has improved from 8% in 2012 to 10% TTM. Longer term, ROIC has improved from 2% in 2004.

Figure 2: Improvement In ROIC Since 2012

Sources: New Constructs, LLC and company filings

We’ve detailed ways in which ROIC is directly correlated to changes in shareholder value here. Plexus’ use of ROIC and ROCE to measure performance ensures executives’ interests are aligned with shareholders’ interests.

PLXS Remains Undervalued Despite Strong Fundamentals

Investors have rewarded PLXS for its profit growth and ROIC improvement and the stock is up 70% over the past five years. This performance is below the S&P 500, which is up 72% over the same time. PLXS remains undervalued.

At its current price of $57/share, Plexus has a price to economic book value (PEBV) ratio of just 1.1. This ratio means the market expects Plexus will grow NOPAT by no more than 10% over the remainder of its corporate life. This expectation seems pessimistic for a firm that has grown NOPAT by 8% compounded annually since 2012.

If Plexus can continue growing NOPAT by 8% compounded annually for the next decade, the stock is worth $74/share today – a 30% upside.

Impacts of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to Plexus’ 2016 10-K:

Income Statement: we made $40 million of adjustments with a net effect of removing $22 million in non-operating expense (1% of revenue). We removed $31 million related to non-operating expenses and $9 million related to non-operating income. See all adjustments made to PLXS’ income statement here.

Balance Sheet: we made $603 million of adjustments to calculate invested capital with a net decrease of $40 million. The most notable adjustment was $94 million (8% of reported net assets) related to goodwill. See all adjustments to PLXS’ balance sheet here.

Valuation: we made $696 million of adjustments with a net effect of increasing shareholder value by $39 million. The largest adjustment to shareholder value was $368 million in excess cash. This adjustment represents 19% of Plexus’ market value.

This article originally published here on February 22, 2017.

Disclosure: David Trainer, Kyle Guske II, and Kyle Martone receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.